Jumping on the bitcoin bandwagon underestimates new technology’s long-term potential

From blockchain to AI, 2017 was the year companies fully embraced jumping on the shiny new tech bandwagon. Bohemia’s Alex Connell considers how our tendency to run before we can walk is affecting businesses.

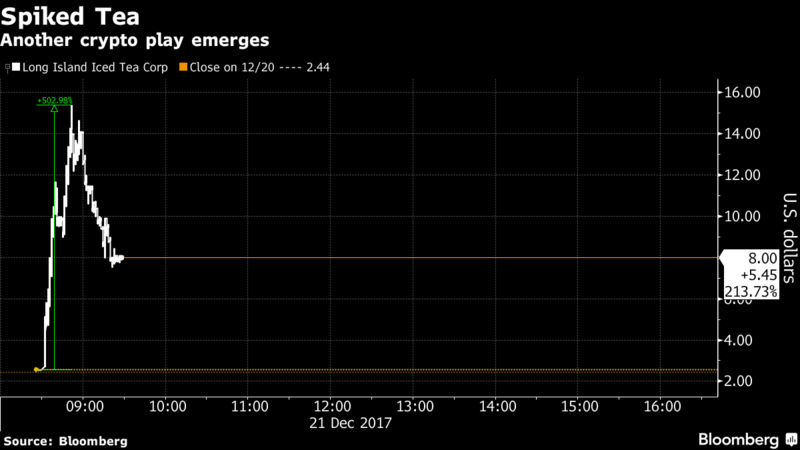

We’re currently living through a time where an ice tea manufacturer can add blockchain to their name and increase their share price 200%, an asset with no perceived value other than market confidence increases its share price from $500 – $18,000 in a year, and supposedly everyone from your local grocer to Amazon is using AI despite not really knowing what it means.

There is no denying it’s a bizarre time not only to be in business but to be alive.

Alex,

This article is classic click-bait garb lacking any real substance on the subject matters of BTC, blockchain or innovation. Instead you have used the term bitcoin as bait to seemingly prove you have read the very old, but classic ‘The Innovator’s dilemma’.

If you haven’t already, I suggest you read the Stratechery blog by Ben Thompson who provides excellent extension and counter-points via his ‘aggregation theory’ to the term ‘innovative disruption’. ‘Disruption’ as Clay defines it from the bottom-up does not always hold true in the modern age (e.g. Uber) (nb. which makes sense given the book was written in 1997).

Further, if you do intend to write another piece on ‘bitcoin’ or ‘blockchain’, can you do some actual research and provide some real substance on the matter.

ps. If you are going to write an opinion piece on innovation, please provide us a unique take, not concepts regurgitated from a book

Hi Disappointing…

1) Sometimes headlines are written by an editor as this one was. I agree it’s quite click-baity.

2) This was never intended to be a thorough analysis into BTC, blockchain or innovation but more to try and give some simple reasoning into why these terms seem to be increasingly used by businesses who don’t really need to be experimenting with new tech.

3) If you’re after an interesting take on innovation, I’d recommend reading Tom Goodwin’s theory of the paradigm leap. It also completely contradicts the Christensen theory, which I agree definitely has holes given the innovations that have happened post 1997.

hey “Mr/Ms Disappointing” did you miss having a holiday? Why don’t you write something of substance as you suggest Alex does rather then shooting someone who’s taken the time to put together a thoughtful read on a current hot topic.

“The canvas of opportunity and the tools to execute have never been greater, but too often it’s brands looking for a quick win with a flashy PR release that taking the headlines and not those willing to undertake vast organisational effort in effort to reimagine what’s possible and want can be solved with the power of technology.”

Is this post about advertising? Very vague and hard to pinpoint what you are actually saying.