Australian ad industry growth to 2023 to be scooped up by internet giants, warns PwC media outlook report

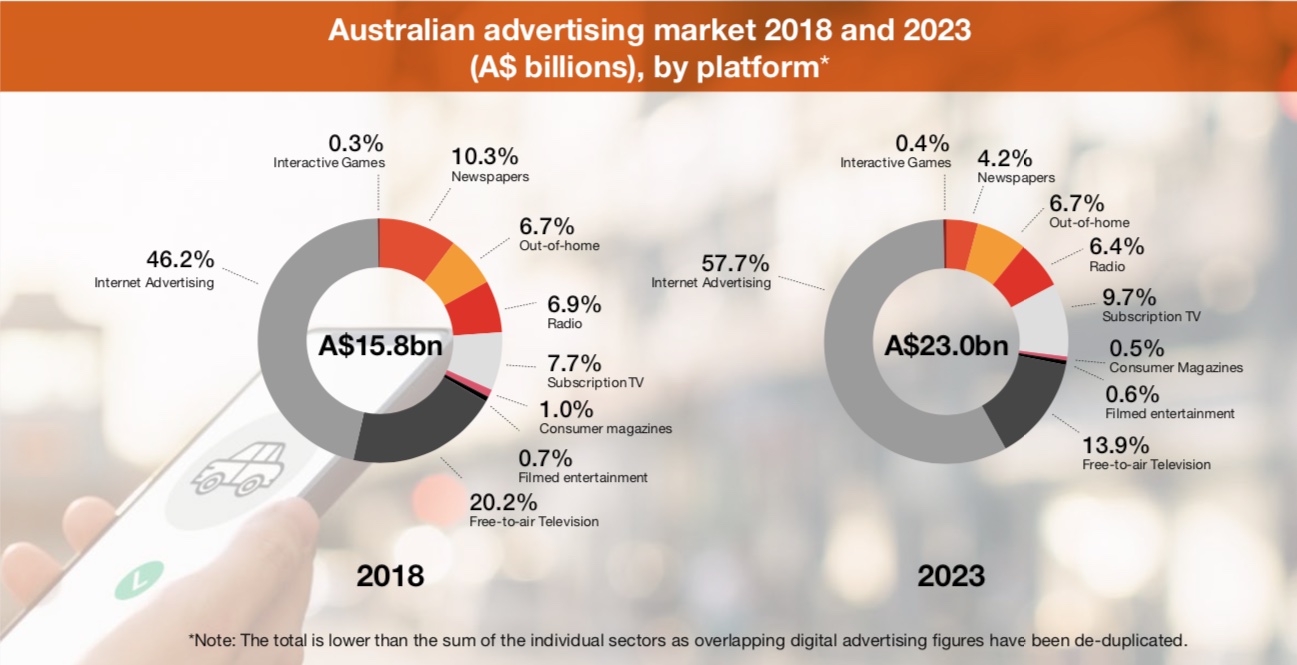

Australia’s advertising industry is expected to grow to $23bn by 2023 with the bulk of growth being taken by internet spending, PwC claims in its latest Entertainment and Media Outlook report.

The report estimates online services will pick up 57.7% of the market in 2023, up from 46.2% in 2018, forcing media owners to look at innovative ways of maintaining revenues.

Were these forecasted numbers simply based on historical ad spending trends or did they factor in any consideration to possible economic downturns??

Consumer spending is tightening up, mortgage stress is on the rise and whenever unemployment reaches it’s lowest and best percentage ever, guess what happens next? That’s right… it starts to get worse.

We have the RBA talking about lowering interest rates in a last ditch attempt to try and stimulate household cash flow and spending, talks of potential quantitative easing. Overseas you have Deutsche bank in trouble with overexposure to derivatives, Brexit, the basket case of Italy, trade wars in the US and also inverted yield curves in the bond market (leading indicator of US recession).

Here’s a forecast for :

2020 and 2021 to see ad spend levels decline massively in alignment with tightening big & small business and household cash flow.

Major job losses in the building sector

Marketing job losses particularly in the big end of town as they try to count more on automation

The FANG tech stocks that have gone parabolic to have the largest market corrections.

The Aussie dollar to continue its decline causing even more pressure on household spending as we no longer produce anything here in Australia

happy hump day! 🙂

This was one of the most impressive presentations I’ve seen in a long time. Progressive, strategic and solid. Lots to take out.

Why ‘warns’ in the headline?

Perhaps leave ‘warns’ in the headline, however superseded with:

warns giant accountancy corporation, best known for helping other corporations to pay the least amount of tax possible…?