Streaming wars: what impact is Stan, Presto and Netflix having on the media landscape?

On the first anniversary of the launch of Stan Nic Christensen speaks with all of the streaming players about how the battle for supremacy is playing out.

Ask Stan boss Mike Sneesby how business is going and you get a response that oozes confidence.

“We’ve had cracker of quarter,” says Sneesby. “The best we’ve had. I look at the things we have done and for us it comes back to the basics.

“Our product has been value for money – everything for $10 a month – and the marketing team has done a phenomenal job of telling everyone about it. That has resulted in an acceleration in brand awareness and then, secondly, in brand sentiment over the year.

“We signed up over 100,000 subscribers in December and we won’t be far off doing that again in January … The confidence of the shareholders and the board’s expectations of me has now turned clearly to the long term,” he explains, “It’s a five-year horizon.”

Sneesby may exude confidence but it’s not that long ago a Citibank report questioned the viability of the business case for Stan, projecting the company to lose just under $200m over the next four years, on an EBITDA basis.

At the time, the report drew a highly critical response from Stan CEO Sneesby, who argued that Citi’s estimates were based on far more conservative subscriber and revenue estimates than what Stan was seeing.

Today the streaming boss is even more ebullient than he was six months ago. Speaking to Mumbrella ahead of today’s anniversary he argues that in the wake of a strong finish to the year – he has been publicly touting a gross subscriber number of 700,000 – and says he is now supremely confident about the future of his business.

In the past 12 months subscription video on demand (SVOD) players such as Stan, Presto and, in particular, Netflix, have impacted substantially on the media landscape. The problem is measuring the precise nature of that impact on a medium like TV.

Rubbery numbers: where are the major SVOD services up to in Australia?

Netflix estimated to have had 300,000 local subscribers before March.

When it comes to the Australian streaming landscape one player looms large: Netflix.

Officially, the global streaming giant launched in Australia last March, well after local services Stan, Presto and Quickflix, but in the eyes of many it is Netflix that really fired the starter’s gun in the race for local subscribers.

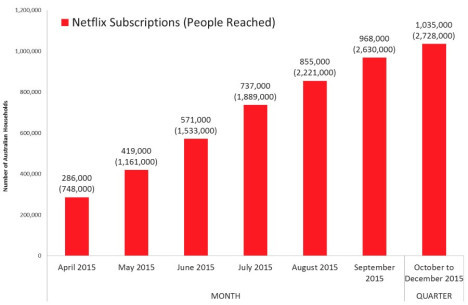

Roy Morgan’s single source survey now estimates Netflix reached and then surpassed one million Australian households at the end of 2015, giving it a reach of 2.7m Australians.

The reliability of the Roy Morgan survey is questioned by local competitors and Netflix, controversially, had the advantage of accessing an estimated 300,000 subscribers who were already using the service via VPN to reach the US. Regardless, all agree that the service has built an impressive local subscriber base in a relatively short amount of time.

The reliability of the Roy Morgan survey is questioned by local competitors and Netflix, controversially, had the advantage of accessing an estimated 300,000 subscribers who were already using the service via VPN to reach the US. Regardless, all agree that the service has built an impressive local subscriber base in a relatively short amount of time.

Netflix itself won’t break out local subscriber numbers but a spokesman for the US-based service told Mumbrella: “Whilst we don’t release numbers territory by territory, we are happy with how Australians have embraced Netflix. We have over 75m members in 190 countries enjoying more than 125m hours of TV shows and movies per day.”

It’s this global strength that dwarfs the likes of Stan and Presto, both of which racing to build a local subscriber base that makes their domestic businesses viable in the long term.

The thing is, many in the streaming space believe that local SVOD players aren’t exactly being transparent about how they’re doing.

PwC’s Brownlow: Netflix is seen as dominant

“It is certainly the view that Netflix is dominant,” says Megan Brownlow, editor of PwC’s Australian Entertainment and Media Outlook report.

“The (problem is the) numbers are all rubbery at the moment and so I wouldn’t want to report any numbers until we get some robust measurement.”

One problem is a lack of consensus on how to measure subscribers. In a panel discussion, at Mumbrella360, Stan was quoting “gross subscribers”, Quickflix was touting “total customers” (which includes its NZ operation and DVD rentals) while Presto has refused to publically reveal a number, despite folding its subscriber base into Foxtel’s overall subscription base.

Related content: Presto, Stan, Quickflix: You need to come clean on your numbers

https://www.youtube.com/watch?v=um0x2Va9gHw

“(We) would love it but the industry players don’t see the need because they are not supported by advertising,” explains Brownlow. “There is no business model imperative to provide a currency around audience. That’s what it is going to be for a while.”

That is certainly the viewpoint of Presto boss, Shaun James, who argues that refusal shouldn’t be seen as a sign of weakness or a lack of confidence in his business’s future.

James: “We are not breaking out our numbers.”

“We are just not breaking them out,” says James. “(When we started the business) we were aware of the fact that one of the things with SVOD services, which has been a historical trend, is that they scale very quickly.

“We are tracking well. We are pretty much on the plan we thought we’d be for the fiscal year,” he explains.

“We had a very solid December, (even though) we haven’t released figures. The figures you release if you are selling ads, and we are not selling ads.”

Stan is somewhat more transparent about its numbers, although its critics will note that its regular touting of so-called “gross sign-ups” has often been interpreted in the media as paying subscribers, which they are not.

“We have passed the 600,000 mark and close to the 700,000 mark gross sign-ups,” says Sneesby. “They are in the front door with credit card down for the service.”

Questioned about how many of those subscribers are sticking with the service in the long term, beyond a one month free trial, he responds: “More than 70% of those gross sign-ups are converting customers.

Questions remain about Stan’s active and paying subscriber numbers.

“What we are seeing is that as a subscriber goes through their life cycle from free trial, 70% are converting to paying and then, through the first seven months, consumer churn is down to sub 2% of our base.”

That 2% figure can potentially misrepresent Stan’s growth with many in the industry noting that churn is calculated monthly, meaning a 2% monthly churn translates to a 24% loss of subscribers over 12 months.

Put more simply many tip that Stan’s active subscriber base is likely to be somewhere between 300,000-350,000 (600,000 x a 70% conversion = 420,000, then deduct 24% churn = 320,000).

Stan disputes this calculation, with Sneesby arguing that the conversion and churn rates can’t be used to extrapolate to a total number.

“What it does tell you is that our conversion to paying subs is very high versus the category and that once a subscriber makes the decision to start paying they become very sticky,” Sneesby says.

Presto, for its part, is harder to estimate given its lack of transparency, although industry consensus appears to be that it trails Netflix and Stan giving it a likely subscriber base somewhere in the order of 200,000-250,000, with the company having aggressively given away a number of three- and six-month subscriptions in order to get Foxtel customers, and others, using the service.

Presto, for its part, is harder to estimate given its lack of transparency, although industry consensus appears to be that it trails Netflix and Stan giving it a likely subscriber base somewhere in the order of 200,000-250,000, with the company having aggressively given away a number of three- and six-month subscriptions in order to get Foxtel customers, and others, using the service.

A multimillion dollar marketing war claims its first casualty

But the question many in the industry are asking is not where the SVOD services are right now but where will they be in one year, two years and five years? And that will depend on marketing budgets and the willingness to persist in the face of short-term losses.

2015 saw major marketing campaigns from Stan and Presto with the likes of Rebel Wilson and Naomi Watts fronting the consumer awareness and brand push.

https://www.youtube.com/watch?v=xP9jYTtC3RA

“We are pleased with the way the brand has grown, we are pleased with the awareness of Presto but we still want to keep pushing very hard,” says James.

“Everyone is marketing as are we,” he adds. “That was part of the business plan, we knew we had to build the Presto brand and build from an educational point of view of what streaming is and how people can access it.

“We had to push forward on the available content on the service. So that will continue; we have been very aggressive in the last 12 months and will continue to be so.”

Indeed Presto and Stan have been very aggressive with TV and digital advertising while Netflix has relied more on digital advertising and a strong word-of-mouth campaign through its global brand, which has generated strong global media around Netflix exclusives like House of Cards Season 4, when it hijacked the Republican primary debate.

https://www.youtube.com/watch?v=Se44ed4KBMA

In March 2015 there were estimates that tens of millions would be spent in the SVOD marketing war, and according to estimates so far more than $30m has been spent, with most of it between Stan and Presto.

Nielsen is putting Stan at the top of the ladder having so far, with an estimated $16.3m (although some of that is likely to be contra through its parent companies Fairfax Media and Nine Entertainment Co.). Presto is estimated to be just behind with $14.8m and Netflix, despite a clear supremacy in market, has only spent $1.795m.

Yet while the full impact of this spending is yet to be seen but it appears there has already been one clear casualty: Quickflix.

Yet while the full impact of this spending is yet to be seen but it appears there has already been one clear casualty: Quickflix.

The Australian owned business was first to market but has struggled in 2015, with a much touted partnership with Presto suddenly aborted, declining subscriber numbers and struggling to match the marketing spends of its rivals, while its share price has been stuck in an ASX trading halt at a tenth of one cent for the last six months.

Related content: Quickflix appears to have given up but what are the lessons for Aussie media?

Langsford: Quickflix doesn’t have the balance sheet of the other players.

CEO Stephen Langsford argues they were unable to match the budgets of their rivals and now, despite a surge in awareness in the sector, must pivot to focus on transactional business, online movie rentals and its still profitable DVD delivery business.

“My view is that it’s a good thing that all the awareness is happening around streaming,” says Langsford.

“But this is a really challenging sector,” he explains. “Clearly Quickflix doesn’t have the balance sheet of the other players so we are going to be playing a different game.

“We have been in a situation where we haven’t been able to spend money on marketing and the like and if we are saying we are only going to keep to the business model around SVOD that would be a different matter but already we are playing in TV on demand, EST (electronic sell through), SVOD and DVDs still.

“There are certainly some great advantages in the EST market because we play in an earlier window particularly when it comes to movies,” he says.

What impact has SVOD had on television?

The real question for the advertising industry however, is what impact have these streaming wars had on traditional television.

The answer to this question varies dramatically depending on who you ask.

Ross: The impact of SVOD is low.

“My perspective is any impact is very very low,” says Liz Ross, CEO of Freeview.

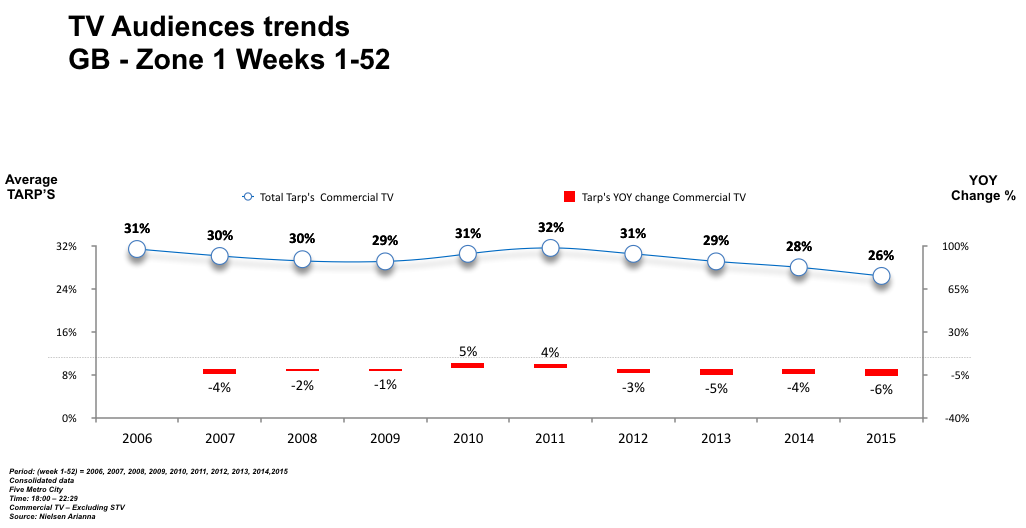

“The question is how you measure that. Looking at the Nielsen report in quarter three last year the average drop only moved by 0.2 of a TARP (target audience rating point – the measurement used to measure reach and frequency in TV audiences by media agencies).

“That’s the average TARP. So overall the outcome is not as great as one might imagine.”

The bosses of Presto and Stan, who are owned by Foxtel/Seven West Media/Network Ten and Fairfax/Nine respectively, also appear to be keen to downplay the impact.

“At the end of the day when people turn their eyeballs to Stan we are clearly taking up their media consumption time but I think the impact is minimal,” argues Sneesby.

“(The reason is) the peak times for our service are in the ‘new prime time’ for SVOD which is after 9pm.

“There is no doubt that free to air is very strong when it hits hardest which is the early evening 6-9.30pm.”

That point is more debatable. Fusion Strategy last year looked at the falls in prime time viewing and showed that peak night live television audiences for 2015 were down 9.15% for the year.

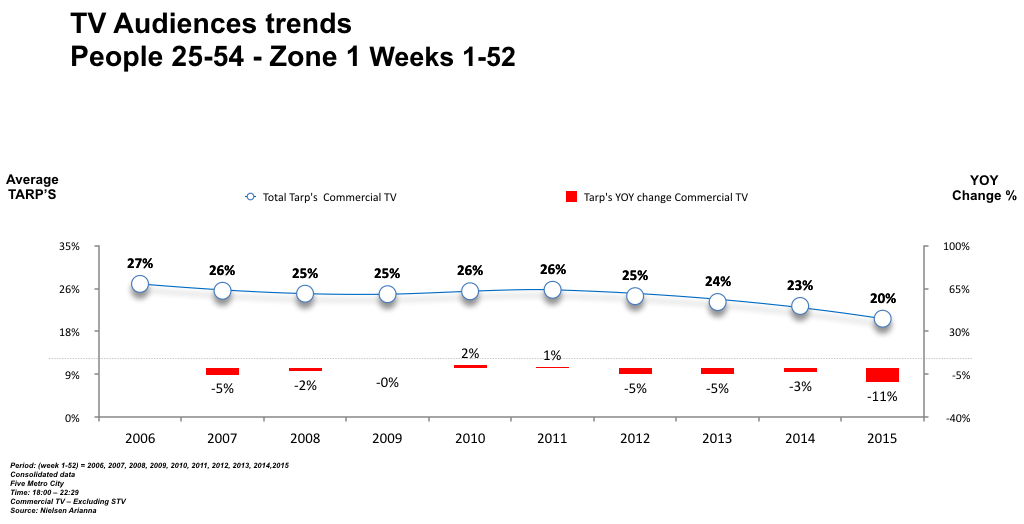

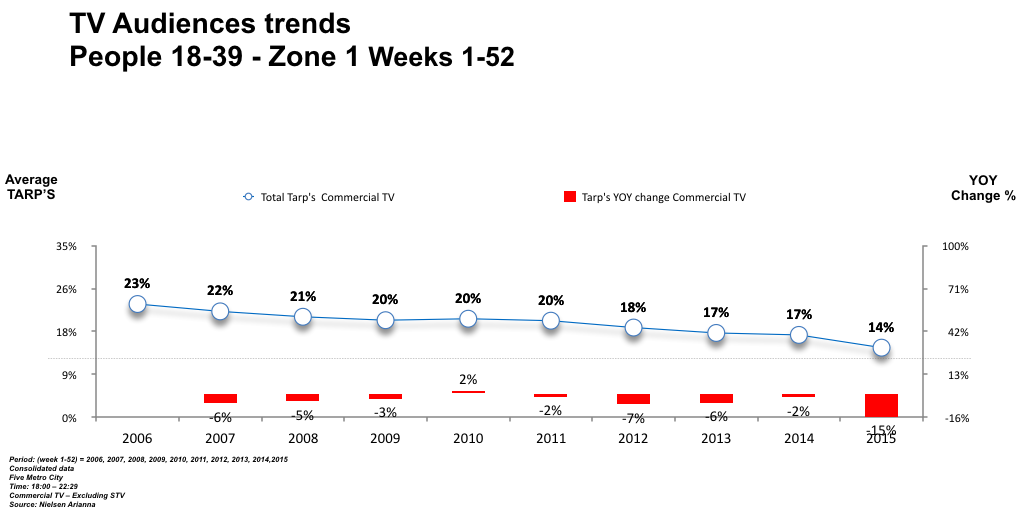

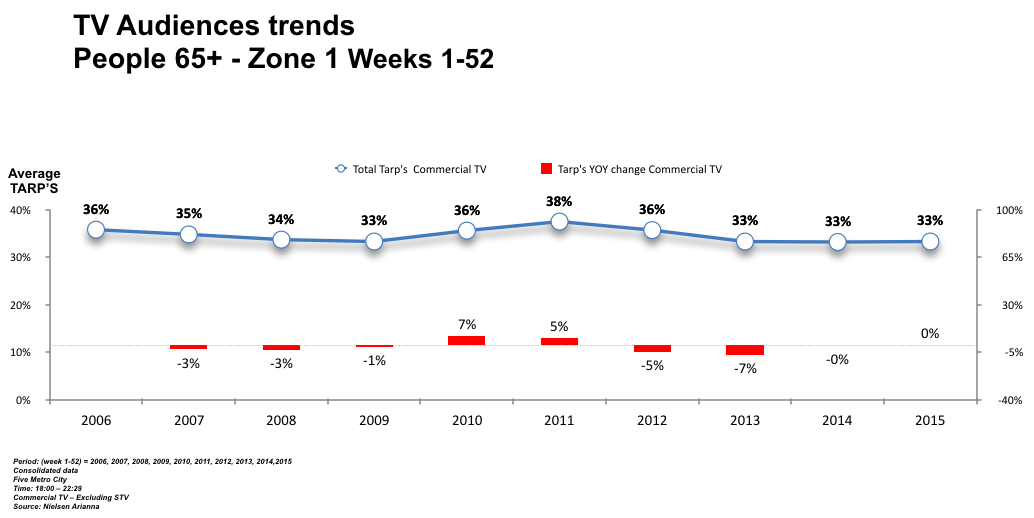

When brought to all important TARP level, upon which media buyers trade, there are very clear falls when you look year on year over the last decade, particularly in key demographics.

One Nielsen analysis of TARPs, obtained by Mumbrella, show that overall TARPs year-on-year for free-to-air TV were down 6%. In the important advertising demographics those declines varied wildly, and the fear among media agencies is that it might be accelerating.

Source: Nielsen data. Click to enlarge.

Among 25-54s they were down 11%, 18-39s were down 15% while those aged 65+ showed no change (full charts at the bottom on this article.)

Scott Lorson, CEO of Fetch TV, a major player in the IPTV platform space aligned to internet service providers Optus, iiNet and Dodo, argues that this is a clear sign of the impact of SVOD but questions whether this is worst of the hit.

Lorson: the main structural hit to TV has already been absorbed.

“Two million households consuming 20-30 hours per month of SVOD content has clearly had an impact on FTA audiences, particularly in the younger demos,” says Lorson.

“We expect SVOD growth rates and hours viewing to temper in 2016, which would suggest the main structural hit to the FTA’s has already been absorbed,” he says.

Media buyers however, worry that this isn’t the case and that there may be more to come.

Ryan: Media buyers eyes are on the Netflix content pipeline.

Simon Ryan CEO of Carat, a media agency which has more than $1.2bn in billings argues Netflix may be a sleeping giant in this streaming war and that the casualties may not be finalised yet.

“If I look at it from a global perspective you have 75m members in 190 countries for Netflix,” says Ryan.

“There’s 14,000 downloadable titles globally and only 1,000 available here and the point is here is that the pipeline is only going to get bigger.

“SVOD and Netflix have clearly had an impact in less than 12 months, but it will have a further impact and it will become more competitive overall – right now we are only getting 10% of their content pipeline.”

Nic Christensen is the media and technology editor of Mumbrella.

Tomorrow Mumbrella looks at what’s next in the Australian subscription video wars.

Full Nielsen TARP charts over 10 years.

Demographics 25-54s.

Click to enlarge.

Demographics 18-39s.

Click to enlarge.

Demographics over 65.

The content on Stan is rather unappealing and outdated. It is a subjective point of view I know, but in my opinion between Stan, Presto and Netflix….it is only Netflix whom provide not only a reliable service, but also an interesting variety of mainstream content. This does not mean that I won’t watch Stan, but they’ve got a bit of work in my humble opinion to navigate a majority audience to them.

User ID not verified.

Yeah, but… you can get all the stuff Stan & Presto have on a Netflix VPN service.

3 vendors in one.

I still don’t see why anyone who has the smarts, would want to pay $30 p/m instead of $13 (of $18.50 USD) inlc. VPN service…. $138 AUD p/year saving…

User ID not verified.

I think Stan will probably survive.

I’m mildly interested in getting it to compliment Netflix but will wait until they have more original content before spending the cash.

User ID not verified.

That’s a fanfiction trailer for House of Cards fyi…

User ID not verified.

Thanks for flagging Andrea,

Now fixed.

Cheers

Nic – Mumbrella

Quickflix was a victim before SVOD even started because of piracy and Australia’s dismal broadband speeds. There is a good article in today’s Australian (28-01) about where SVOD could be heading with Global Alliances being formed by local players in each country and hopefully this may lead to an end to Geo-Blocking which has no place in a Global internet.

User ID not verified.

errr…. none of the charts open on the Click to enlarge option. Cheers.

User ID not verified.

Thanks for picking up on that. Files have been fixed.

How much harm is it doing to the Presto brand, being associated with Foxtel? The main reason for many people are choosing SVOD is because it’s not Foxtel. Whilst price, content and technology are probably more important than brand perception it does influence consumers. I don’t have a single mate who thinks Foxtel offers value for money and puts the customer first and that perception does rub off on Presto regardless of how good the service is.

User ID not verified.